Raising and caring for a loved one with a disability comes with unique joys, challenges, and responsibilities. For many families, one of the most difficult questions to answer is: How do we make sure they’re taken care of, even after we’re gone?

Special needs financial planning isn’t just about money—it’s about building peace of mind. It requires thoughtful coordination between legal, financial, and tax strategies to ensure your loved one maintains access to benefits, receives appropriate care, and is supported well into adulthood.

This guide outlines the key components of an effective financial plan for families with a child or dependent with special needs.

The Financial Landscape of Special Needs Planning

According to national estimates, the lifetime cost of care for an individual with disabilities can exceed $1 million—especially when accounting for housing, therapies, education, personal care, and lost earnings.

These expenses are further complicated by the need to preserve eligibility for critical public benefits like Supplemental Security Income (SSI) and Medicaid, which are means-tested. That means a well-intended financial gift or inheritance could jeopardize your loved one’s access to services if not handled correctly.

The good news: with the right structure in place, you can provide long-term support and protect eligibility.

What Is a Special Needs Trust (SNT)?

A Special Needs Trust is a legal arrangement that allows you to set aside money or property for the benefit of a person with disabilities without disqualifying them from public assistance.

There are two primary types:

1. First-Party SNT: Funded with the individual’s own assets (e.g., an inheritance, legal settlement). Any remaining funds at death typically go to the state as repayment for Medicaid benefits.

2. Third-Party SNT: Funded by parents, grandparents, or others. No payback requirement to the state, and can direct remaining funds to other heirs.

SNTs allow funds to be used for:

- Medical and therapy expenses

- Education and training

- Travel and recreation

- Assistive technology

- Personal care aides

But not food or shelter expenses—those could reduce SSI payments.

Choosing a trustee is one of the most important decisions you’ll make. The trustee ensures funds are used appropriately and in compliance with federal and state laws.

ABLE Accounts: A Flexible Complement

Introduced under the Achieving a Better Life Experience (ABLE) Act, ABLE accounts are tax- advantaged savings accounts for individuals with disabilities who were diagnosed before age 26.

Key features:

- Up to $18,000/year in contributions (as of 2024)

- Tax-free growth and withdrawals for qualified expenses

- Account balance under $100,000 does not affect SSI eligibility

Qualified expenses include housing, education, job training, transportation, assistive technology, and more.

When are ABLE accounts helpful?

- To allow the individual to manage some of their own money

- To use for everyday qualified expenses

- As a complement to a trust for smaller, more flexible spending

-

Keep in mind: not all states offer ABLE plans, but many plans are open to out-of-state residents.

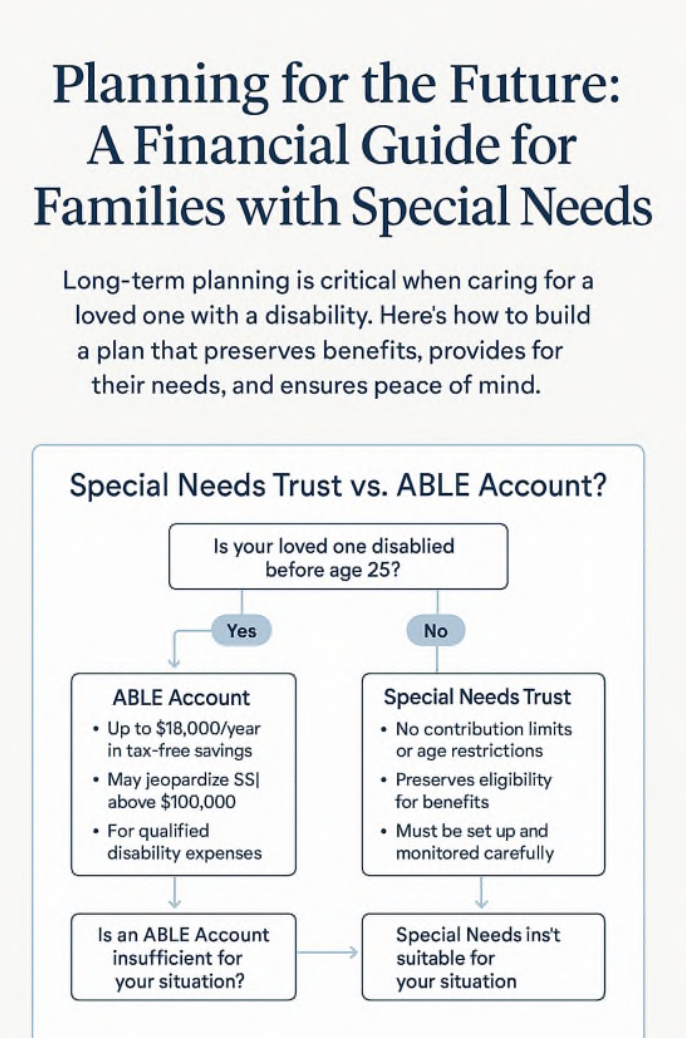

When to Use an SNT vs. ABLE Account

To help illustrate the decision, here’s a quick visual guide:

1. Was the disability diagnosed before age 26?

↓

Yes → ABLE Account may be used (next question)

No → Consider Special Needs Trust only

2. Will annual contributions exceed $18,000 or total assets exceed $100,000?

Yes → Use SNT or both

No → ABLE account may be sufficient for now

3. Do you want more control, flexibility, and legacy planning options?

Yes → Consider SNT as primary vehicle

More Than Just Legal Documents: A Holistic Plan

Even the best-drafted trust or ABLE account isn’t enough on its own. A complete plan includes:

- Letter of Intent: A non-binding document that outlines your loved one’s history, preferences, routines, and needs—a personal guide for future caregivers.

- Guardianship or Power of Attorney: Depending on capacity, you may need to petition for guardianship or have your child execute powers of attorney at age 18.

- Life Insurance: Often used to fund a trust without diverting assets needed for retirement or other children.

- Housing & Education Planning: Evaluating programs, group homes, schools, and future care settings.

These elements evolve over time. Your plan should too.

How Wealthquest Simplifies Special Needs Planning

Coordinating tax strategies, legal structures, and investment decisions is hard enough under normal circumstances. Add in the complexity of special needs planning, and it can feel overwhelming.

That’s why Wealthquest’s All Under One Roof model is such a differentiator.

Our in-house financial advisors, CPAs, and estate planning partners work together as one team to design a fully integrated plan. We make sure your Special Needs Trust is funded properly, your tax returns reflect those strategies, and your legacy goals are honored across generations. With multiple CPAs on staff, we don’t just create the strategy—we execute it with accuracy, cost-efficiency, and long-term vision.

Final Thoughts: Start the Conversation

You don’t need to have everything figured out to begin. The most important step is getting started.

Whether you’re updating an existing estate plan or planning for the first time, our team can help you build a strategy that reflects your values and safeguards your loved one’s future.

If you’re navigating the complexities of special needs planning, schedule a conversation with Wealthquest today. Our coordinated team of financial advisors, CFPs and CPAs will guide you through every step to create a plan that gives you peace of mind today and

security tomorrow.

For informational purposes only. Past performance is not indicative of future results. Investing involves risk, including the possibility of loss of principal. Wealthquest Corporation (“Wealthquest”) is an SEC registered investment adviser. Registration as an investment adviser does not imply a certain level of skill or training. The ideas and opinions expressed herein do not constitute legal, tax, or investment advice or a recommendation of any particular security or strategy. Before making any investment decision, you should seek expert, professional advice and obtain information regarding the legal, fiscal, regulatory and foreign currency requirements for any investment according to the laws of your home country and place of residence. Any forward-looking statements or forecasts are based on assumptions and actual results may vary. Information presented from third parties is believed to be reliable, but no warranty is provided. Wealthquest is not required to update information presented, unless otherwise required by applicable law. For more information about Wealthquest, including our Form ADV Part 2A Brochure, please visit https://adviserinfo.sec.gov/firm/summary/141473 or contact us at 513-530-9700